Understanding the Home Loan Process

Getting a home loan in Bangalore feels overwhelming. Between bank websites, interest rates, and endless documentation – most people get stuck before they even start.

Here’s the reality: Understanding the home loan process isn’t complicated. It’s just 8 straightforward steps. And once you know them, you’ll make smarter decisions that save lakhs of rupees.

A Story Many Bangalore Home Buyers Experience

Meera and Arun found their dream home in Sarjapur Road. ₹80 lakhs. They approached HDFC Bank and got quoted 8.5%.

Without comparing, they started the home loan process. Documents, valuations, approvals happened.

Then Arun’s colleague mentioned: “I got 7.9% from ICICI last month. Negotiated to 7.7%.”

On an ₹80 lakh loan, that 0.8% difference meant ₹60 lakhs more in total interest over 20 years.

They learned too late: The home loan process isn’t just about getting approved – it’s about comparing every bank and negotiating every rate.

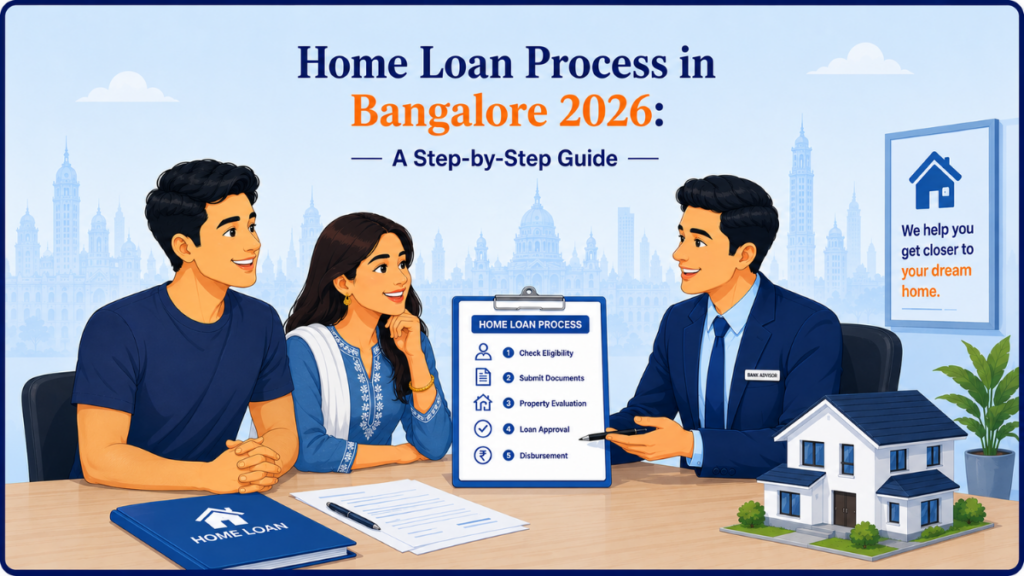

How the Home Loan Process Works: 8 Steps

Step 1: Check Your Eligibility

Before you visit a bank, know if you qualify.

Basic Requirements:

- Age: 21-65 years

- Income: ₹25,000+ monthly (salaried) or ₹3+ LPA (self-employed)

- CIBIL Score: 750+ for best rates

- Employment: 2+ years in current job

Quick Check: If your monthly income is ₹1,00,000, you can comfortably borrow up to ₹80 lakhs (with 20% down payment).

Step 2: Gather Home Loan Requirements Documents

This is the tedious part. Banks need proof of everything.

What You’ll Need:

Income Proof:

- Last 2 years’ salary slips and ITR

- 6 months’ bank statements

Property Documents:

- Sale deed, approved plan, tax receipt

- Occupancy certificate (for ready property)

Identity & Address:

- Aadhaar, PAN, recent utility bill

Financial Documents:

- 6 months’ bank statements

- Other loan details

Start gathering these 2 weeks before applying. This speeds up the entire home loan process.

Step 3: Compare Banks and Interest Rates

This is where most people fail. They pick one bank without comparing.

Current Home Loan All Banks Interest Rates in Bangalore (May 2026):

| Bank | Rate | Processing Fee | Speed |

| SBI | 8.15% – 8.65% | 0.40% – 0.50% | 7-10 days |

| HDFC Bank | 8.40% – 8.80% | 0.50% – 0.75% | 5-8 days |

| ICICI Bank | 8.25% – 8.75% | 0.50% – 1.00% | 5-7 days |

| Axis Bank | 8.35% – 8.85% | 0.50% – 0.75% | 7-10 days |

| LIC Housing | 8.35% – 8.85% | 0.30% – 0.50% | 10-15 days |

| Federal Bank | 8.30% – 8.80% | 0.50% – 0.75% | 8-12 days |

Key insight: A 0.5% rate difference = ₹10-30 lakhs saved over 20 years. Compare at least 3 banks.

Step 4: Apply and Get Approval

Submit your documents to the bank. They’ll verify everything and check your CIBIL score.

Timeline: 3-5 working days for initial review.

The bank then orders a property valuation. This is crucial – the valuation determines how much they’ll lend you.

Step 5: Property Valuation

A bank valuator visits your property to assess its market value. This affects your loan amount directly.

If valued lower than purchase price: Your loan reduces proportionally. You need to increase your down payment.

Timeline: 3-7 days.

Step 6: Final Approval

After valuation, the underwriting team reviews everything. Credit appraisal happens. Then approval.

You get a commitment letter. This is when the home loan process feels real.

Timeline: 5-10 working days.

Step 7: Documentation and Signing

You visit the bank and sign:

- Loan agreement

- Promissory note

- Mortgage deed

Read everything carefully. You’re signing for 20 years.

Step 8: Disbursement

Money lands in your account. Your home loan process is complete. Your EMI journey begins.

Timeline: 3-5 working days after signing.

What You Need to Know About Low Home Loan Interest Rates

Everyone wants a low home loan interest rate. But what actually gets you one?

Factors That Get You the Best Rates:

1. CIBIL Score (Biggest Impact)

Your CIBIL is your credit reputation. Banks instantly know your creditworthiness.

- 800+: Lowest rates (base – 0.25%)

- 750-799: Good rates (base rate)

- 700-749: Standard rates (base + 0.25%)

- Below 700: High rates or rejection

Action: If below 750, improve it before applying. Takes 3-6 months.

2. Down Payment

More money upfront = lower interest rates.

- 20% down: Standard rate

- 30% down: 0.25% discount

- 40% down: 0.50% discount

3. Loan Amount

Larger loans get better rates. Banks prefer bigger deals.

4. Employer

Work at Google, Infosys, Amazon? Banks love you. Expect 0.25-0.50% better rates.

5. Existing Bank Relationship

If you bank with them already (salary account, investments), you get low interest on home loan benefits.

Real Example:

Priya (CIBIL 780, Google employee, ₹2 crore property, 40% down, HDFC customer):

- Without negotiation: 8.40%

- With benefits: 7.95%

- After negotiation: 7.75%

Result: ₹45 lakhs saved over 20 years.

Fixed vs Floating: Which Should You Choose?

Fixed Rate

Your rate stays the same for the entire tenure (15, 20, or 25 years).

Pros: Predictable EMI, peace of mind, better for budgeting

Cons: Starts 0.5-1% higher, no benefit if rates fall

Current Rate: 8.75% – 9.00%

Floating Rate

Your rate changes with RBI repo rate. When RBI raises rates, your EMI increases.

Pros: Starts lower, benefit if rates fall

Cons: Unpredictable, EMI can jump, harder to budget

Current Rate: 8.15% – 8.40%

Which to choose? If you want certainty and budget stability, go fixed. If you have a good income buffer and can handle changes, go floating.

Home Loan Guidelines RBI: What Protects You

RBI has strict rules to protect borrowers. Know these.

Key RBI Guidelines:

- Loan-to-Value (LTV): Maximum 80–90% of property value (you need 20–10% down payment)

- EMI Cap: Monthly EMI shouldn’t exceed 60% of gross income

- No Prepayment Penalty: You can repay anytime without penalty (RBI law)

- Tenure: Maximum 30 years (or until age 70)

- Floating Rate Protection: Banks must inform you of rate changes within 2 weeks

- 7-Day Cancellation: You can cancel the loan within 7 days of getting the commitment letter

If a bank violates these, report to the RBI Ombudsman (free).

Real Bangalore Scenarios

Scenario 1: Ready Property in Whitefield (₹80 lakhs)

| Bank | Rate | EMI (20 yrs) | Total Interest |

| SBI | 8.35% | ₹48,850 | ₹37.2 lakhs |

| ICICI | 8.55% | ₹49,450 | ₹38.7 lakhs |

| LIC Housing | 8.50% | ₹49,250 | ₹38.2 lakhs |

Strategy: Get 25% down (₹20 lakhs) to negotiate better rates. Monthly outgo: ₹49,000 + property tax (₹1,500) = ₹50,500

Scenario 2: Construction Loan Home in Sarjapur (₹1.2 crore)

Construction Loan Home works differently. Bank disburses in stages as construction progresses.

- During Construction (3 years): You pay interest only on disbursed amount

- After Possession: Converts to regular home loan

- Interest Rate: 0.50% lower during construction phase (7.85% – 8.35%)

Benefit: You only pay interest on what’s disbursed, not the full amount. Saves ₹15-25 lakhs.

7 Things Every Bangalore Home Loan Borrower Must Know

1. Negotiate Before Signing

The best time to negotiate is when the bank approves you and sends the commitment letter. Once signed, you’re locked in.

2. Real Cost Is More Than Interest

Processing fee (0.40-1%), valuation (₹5,000-15,000), legal (₹10,000-25,000), insurance (₹15,000-40,000 annually). Total real cost is 10-15% more than just interest.

3. CIBIL Score Matters More Than Salary

A ₹5 LPA earner with 800 CIBIL gets better rates than ₹20 LPA with 650 CIBIL. Creditworthiness > income.

4. Bank Valuation Can Reduce Your Loan

If the bank evaluates at ₹75 lakhs but you’re paying ₹80 lakhs, your loan reduces. You can challenge yourself with independent valuation.

5. Floating Rates Can Spike Your EMI

A 1% rate increase = ₹300-500 more EMI monthly. Over 20 years, that’s ₹78 lakhs extra interest. Plan for this.

6. RBI Prohibits Prepayment Penalties

You can repay anytime without penalty. This is RBI law. If a bank charges it, report them.

7. Claim Tax Benefits

Section 24 (interest deduction) + Section 80C (principal deduction) = ₹1-2 lakh tax savings annually. Don’t miss this.

How Agarwal Estates Helps You Navigate Home Loans

When buying property in Bangalore, the home loan process is critical. One wrong decision compounds for 20 years.

Agarwal Estates doesn’t just list properties. They guide families through the entire home loan process with complete transparency.

With 13+ years in Bangalore’s real estate, they help you:

- Compare all banks (not just one) and negotiate the best rates

- Understand total cost of ownership (not just interest)

- Verify property documents for legal clarity

- Navigate RBI guidelines to protect yourself

- Identify high-growth areas that appreciate over time

- Manage the entire transaction from loan to registration

As one client, Tapan Agarwal, shared: “Agarwal Estates explained the pros & cons of fixed, floating, and hybrid loans. They have excel sheets to compare TCO across banks. Best part-they don’t push any particular bank. They explain objectively.“

This kind of neutral, expert guidance is rare. It’s the difference between a property purchase and a smart investment.

Previously written blogs on home loans by us –

- A Comprehensive Guide to Home Loan Documentation: Simplifying Your Journey to Peace of Mind

- How long does it take to process a Home Loan?

- What factors should be considered while applying for a home loan?

- Home Loans – Your One-Stop Checklist and Pro-Tip Sheet

Final Thoughts

The home loan process might feel complicated. But it’s actually 8 logical steps.

Understanding every step gives you power to negotiate better rates, save lakhs, and make confident decisions that feel right for 20 years.

Because in Bangalore’s booming market, the families that win aren’t the ones who move fastest. They’re the ones who move smartest.

And smart means understanding every option, every number, and every home loan process step.

Frequently Asked Questions

Q. What’s the current best low home loan interest rate in Bangalore?

As of May 2026, rates range from 8.15% (SBI) to 8.95% (some NBFCs). Your actual rate depends on credit score, down payment, and negotiation. Get quotes from 3+ banks.

Q. How long does the home loan process take?

Typically 8-15 working days from application to approval. Add 3-5 days for disbursement. Plan 2-3 weeks total.

Q. Can I get loan approval with CIBIL below 700?

Yes, but with 0.75-1.5% higher rates and stricter conditions. Better to improve your score first (3-6 months).

Q. What are the home loan requirements documents I absolutely need?

Minimum: 2 years’ income proof, 6 months bank statements, property documents, Aadhaar, PAN, recent utility bill. Your bank will confirm the exact list.

Q. How much can I save by negotiating low interest on home loan rates?

For every 0.5% reduction: ₹50 lakh loan = ₹8-10 lakhs savings over 20 years. Negotiation is absolutely worth it.

Q. What’s the difference between fixed and floating rate low interest on home loan?

Fixed: Rate stays the same for 20 years (stable but higher). Floating: Changes with RBI rates (lower initially but unpredictable). Choose based on your comfort with change.

Q. Does construction loan home have different home loan all banks interest rates?

Yes, 0.50% lower during the construction phase (7.85-8.35%). Converts to regular rates after possession.

Q. What home loan guidelines RBI protect me from overcharges?

No prepayment penalty, max 60% debt-to-income ratio, transparent fees, 7-day cancellation period. If violated, report to the RBI Ombudsman.

Q. Can I apply for the home loan process if I’m self-employed?

Yes, but you need 3+ years of business history, consistent profit, and clear ITR. Rates might be 0.25-0.5% higher.

Q. Should I choose a fixed or floating rate for low interest on a home loan?

Fixed: If you want certainty and expect rates to rise. Floating: If you have an income buffer and expect rates to fall.

Q. How do I find a bank with low home loan interest rate in Bangalore?

Compare rates across SBI, HDFC, ICICI, Axis, and LIC Housing. Then negotiate—mention competitor quotes to your preferred bank. A 0.5% discount is realistic if you have good credit, higher down payment, and existing relationship with the bank.

Disclaimer: This article is intended for general informational purposes only and is based on publicly available information as of May 2026. While Agarwal Estates strives to provide accurate insights about the home loan process, interest rates, and home loan guidelines of RBI, we do not guarantee completeness or accuracy. Interest rates, bank policies, and RBI guidelines change frequently. Readers are advised to verify current rates directly with banks, consult qualified financial advisors, and review official RBI circulars. We do not accept liability for errors or outcomes from using this information.